The book was extremely en lighting on many more topics beyond just the crisis of the day

in mortgages and banks. The failures of Freddie and Fannie, Lehman Brothers, Bear Sterns, Citibank and others are merely symptoms of far deeper structural problems with our economy and our collective personal behavior as a society. For example:

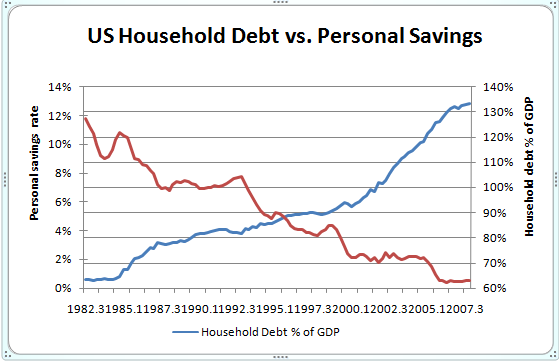

1. We stopped saving and started borrowing so that we could spend more than we earn.

Just take a look at this chart from the book:

2. As a nation, we have gone from being a lender to a borrower, and a borrower on a massive scale.

We have stopped producing products that other countries want to buy, and instead are borrowing trillions of dollars from other countries in order to buy their products. This chart shows the percent of US Treasury bonds held by foreign countries, indicating how far in debt we are getting in order to finance our spending.

Because Americans are not saving and producing but are borrowing and consuming, we have become precariously dependent on foreign suppliers and lenders. As a result, we a facing and imminent monetary crisis that will dramatically lower the standard of living of Americans who fail to protect themselves.

3. We are printing money like there's no tomorrow.

How is it that the government can simply print money, as much as it wants with no limit? The answer lies in the history of money in the United States, in which the dollar began as a paper representation of an amount of gold metal, and gradually morphed into what is called fiat currency. From Wikipedia:

The terms fiat currency and fiat money relate to types of currency or money whose usefulness results not from any intrinsic value or guarantee that it can be converted into gold or another currency, but instead from a government's order (fiat) that it must be accepted as a means of payment.In other words, fiat money is worth something only because the government has decreed that is is worth something. The US dollar is a fiat currency, and therefore is not worth anything in and of itself. It's just paper with ink, so there's not really any practical limit to how much of it can be printed.

There is a very interesting section of the book that explains the origin and history of the US dollar. Money is provided for in the US Constitution where is says: "Congress shall have the power to coin money and regulate the value thereof," meaning that it was empowered to take gold and sliver, which the country then recognized as money, and issue them in the form of coins. Article 1, Section 10 of the US Constitution forbids stats from accepting anything other then gold or silver coin legal tender for payment of debts.

The dollar was first defined in the Mint Act of 1792 as 371.25 grains of fine silver. The first US currency was issued in 1863 as a gold certificate that read "The certifies that there have been deposited in the Treasury of the United States ten dollars in gold payable to the bearer on demand."

The first step in detaching money from tangible assets (thus paving the way for today's situation in which the Federal Reserve Bank arbitrarily prints money backed by nothing) was the Federal Reserve Act of 1913. That act established the Federal Reserve System, which is politically independent of Congress and the President, to supervise the banking system and manage the supply of money. One of their first actions was to introduce a currency called Federal Reserve notes, which were redeemable "in gold or lawful money" at any Federal Reserve bank, meaning gold or silver, as before, but now also Treasury notes. This was the beginning of removing any connecting between money and gold.

The 1934 Gold Reserve Act removed the word gold from Federal Reserve notes, and changed the wording to "This note is legal tender for all debts, public and private, and is redeemable for lawful money at the United States Treasury, or at any Federal Reserve Bank." A subtle change, but now any reference to a connection between paper money and gold was removed.

From the book:

On November 2, 1963, the redemption clause was eliminated completely, rendering all US currency intrinsically worthless. On that date, our monetary system was transformed from the gold-and silver-based system specified in our Constitution to one of government fiat.

...The bottom line is that rather than representing legitimate IOUs redeemable in specified weights of gold or silver, US Federal Reserve notes because IOU nothings, mere pieces of paper that bearers did not constitute any liability on the part of the issuer.

What that meant was that any value the dollar had would depend purely on its purchasing power, which in turn would depend on the financial strength of the US economy and how the supply of dollars was regulated.

So the value of the dollars in our bank account depend on two things:

- the financial strength of the US economy

- how the supply of dollars is regulated

The financial strength of the US economy? Not good right now.

How are the supply of dollars being regulated? Well, because the Federal Reserve can print money without being limited to the amount of gold in its vaults, there's not limit. And haven't recent events proven that the government can simply print money at will?

- $700 billion dollar bailout for banks

- $85 billion bailout for AIG

- Another $300 billion bailout for Citibank

- Auto makers want another $30 billion

Where is all this money coming from? The amount of tax money the government isn't going up. Even if we raise tax rates, it will still go down because people who don't have a job don't pay taxes.

The money is coming from the government printing presses. The total am out of money circulating in the US has increased 20-fold since 1980, from around $500 billion to over $10 trillion, as shown in this chart:

There are many other massive structural problems with out economy as described in the book, including inflation, the size of our national debt, and the amount of money we have promised to people that has no source of funding, such as Social Security, medicare, veterans benefits. Our national debt is $8.5 trillion dollars, and our unfunded promises is over $50 trillion. How much money is that really? Hard to say because numbers that large are abstract. But to me, it seems clear that these are amounts of money we cannon possibly repay.

Inflation is a much bigger problem than official government figures are letting on. Mr. Shiff explains that official government figures on inflation are bogus for several reasons. One, if a product like a car goes up by 10% one year, the government can decide that the car is 20% better due to new features etc, and then say that the car has actually decrease in price, not increased. Second, food and fuel costs, and housing costs, are not included in official inflation statistics. Mr Schiff asserts in the book that inflation is already a much bigger problem than is commonly assumed, and is going to get much worse due to the way we are borrowing and printing money.

So given all of the above, I have to conclude that our economy has been run into the ground, and is a total basket case, destined for a big fall. The events we have seen to date are probably only the beginning of the unraveling. How this economic disaster will play out, and what we can each due personally to prepare for it, is the final section of Mr. Schiff's book and which I'll summarize in the next blog post.